Domestic Debt in Africa: Opportunity or Risk?

Context

In 2002, we published a paper analyzing the choice between domestic and external financing of budget deficits (Loko et al., IMF WP 02/079). Considering the sharp rise in public debt over the past decade, our first blog examined public debt management—particularly how countries can use debt responsibly to avoid excessive indebtedness (Debt: Public Enemy Number One in Africa?). We underscored that while poorly managed debt can hinder growth, well-managed debt can be a powerful tool to finance development and reduce poverty.

In this new blog, we turn our attention to domestic debt. What risks does it pose, and how can they be mitigated?

To meet growing development needs and offset declining external financing—especially official development assistance—African countries have increasingly turned to domestic borrowing. Key trends illustrate this shift:

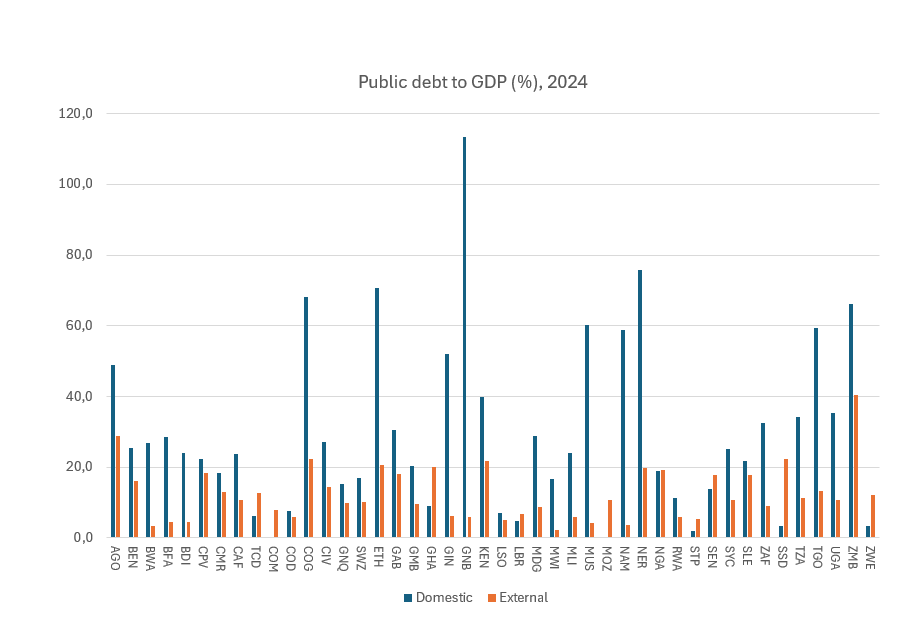

- Across Sub-Saharan Africa, domestic debt rose from 6.7% of GDP in 2016 to 14.9% in 2024.

- In several countries, it now represents nearly one-third of GDP.

- In 2024, domestic debt exceeded external debt in almost half of the region’s 44 countries.

While this shift can reduce external dependence and mitigate vulnerability to international shocks—such as fluctuations in aid, financial markets, or exchange rates—it also raises significant fiscal and financial stability concerns. As the IMF recently noted (Global Financial Stability Report, October 2025, Chapter 3), the growth of domestic financing must be accompanied by heightened vigilance.

Macro-Financial Risks of Rising Domestic Debt

Pressure on domestic financial markets

Heavy reliance on domestic borrowing increases the demand for local capital, potentially driving up interest rates and crowding out credit to the private sector.

Higher fiscal costs

Domestic borrowing is typically more expensive than concessional external financing. As a result, interest payments rise, reducing fiscal space for social spending and investments. In many countries, domestic debt service now consumes roughly one-quarter of public revenues, and in more than three-quarters of countries, it exceeds external debt service.

Increased sovereign-bank contagion risk

Growing sovereign-bank nexus heightens systemic risk through:

- Potential losses on government portfolios during fiscal stress.

- Risks associated with implicit government guarantees.

- Simultaneous deterioration of sovereign solvency and bank asset quality during macroeconomic shocks.

Pressure on international reserves

A significant share of public spending, especially investment, depends on imports. Without sufficient external financing, increased domestic borrowing can erode foreign reserves, exacerbating pressures on the exchange rate and inflation.

What can be done to ensure sustainable development financing?

The rapid rise of domestic debt reflects adaptation to declining external financing. Yet it poses important challenges for fiscal sustainability and macroeconomic stability. Preserving these balances while improving the business environment is essential. Several measures can help mitigate the risks associated with rising domestic debt:

Strengthening public financial management

- Reinforce the legal and institutional framework for fiscal management.

- Increase domestic revenue mobilization.

- Improve efficiency and quality of public spending.

- Enhance governance and transparency.

- Adopt prudent fiscal policies to contain deficits.

- Modernize cash-management systems.

- Reduce domestic arrears to limit and NPL price pressures, liquidity problems and non-performing loans (NPLs) in the banking sector.

Enhancing domestic debt governance

- Publish regular, comprehensive reports on public debt.

- Strengthen risk-analysis capacities and debt-issuance strategies.

Diversifying domestic financing and strengthening financial markets

- Improve regulations.

- Broaden the investor base beyond commercial banks.

- Develop secondary bond markets.

- Promote innovative instruments (green bonds, diaspora bonds, etc.).

- Enhance the banking sector, including by addressing “zombie banks” which are sources of macroeconomic fragility.

- Adopt sound monetary policy frameworks and encourage financial savings.

Key Takeaways

In our previous blog, we emphasized that poorly managed debt can hinder growth, whereas well-managed debt can be a powerful lever to finance the future and reduce poverty.

This analysis shows that domestic debt, while reducing external dependence, introduces challenges related to cost, financial stability, and macroeconomic management.

The choice between domestic and external debt is not only a question of interest rates—it also shapes policy decisions and structural reforms necessary to limit negative effects.

A robust fiscal framework, strengthened debt governance, enhanced banking regulations and diversified domestic financing are key pillars of a sustainable strategy.

In our next blog—echoing our 2002 paper—we will revisit the parameters for optimizing the financing mix between domestic and external sources to reduce risks and preserve debt sustainability.

Debt : Public Enemy Number One in Africa!

African debt often raises concern and misunderstanding. Yet it primarily reflects an unavoidable reality: African countries must invest to drive development — infrastructure, education, health, energy, and more.

So, is the situation truly alarming? And more importantly, how can more resources be mobilized to lift people out of poverty sustainably, without falling into a debt spiral?

Excessive debt… or simply misunderstood?

After the major debt relief initiatives of the 2000s (HIPC Initiative), debt levels have risen again — yet remain below pre-relief levels:

- External debt: USD 807bn in 2024 (+50% in 9 years)

- External debt-to-GDP: 31.5% (2016) → 44.2% (2024)

- Public debt-to-GDP: 38% (2016) → 59% (2024)

Source: IMF, WEO

The real challenge lies not in the stock of debt — lower than in many emerging and advanced economies — but in the cost of servicing it, driven by:

- Lower official development assistance

- Greater reliance on expensive domestic and private financing

- Rising principal repayments on external debt: USD 66bn (2016) → USD 100bn (2024)

- Limited fiscal capacity to absorb the burden

A genuine warning for policymakers

- More than one-third of government revenues are now devoted to debt servicing —

limiting spending on essential services such as education, healthcare, electricity, and roads. - In Sub-Saharan Africa, about 20 countries are already in debt distress or at high risk

(IMF & World Bank assessments).

How to finance development without over-indebtedness?

Four key strategic levers to finance sustainable development:

- Sustained and inclusive growth- Macroeconomic stability, structural reforms, strong governance, efficient public investment.

- Stronger domestic revenue mobilization- Modernized and reinforced tax systems, digitalization, a broader tax base, and more effective oversight of tax expenditures.

- Transparent and responsible debt management- Better risk monitoring and prioritization of high-return investments.

- Enhanced international support- Stronger restructuring mechanisms, increased concessional financing, mobilization of private capital.

The real battle: reducing poverty

The continent’s future is not threatened by debt itself, but by insufficient investment, still-fragile economic governance, and slow structural reforms to improve living conditions: nearly one in two Africans lives on less than USD 3 per day (World Bank).

Poorly managed debt can weigh on growth; but well-managed debt is a powerful engine for development and poverty reduction (Loko et al., IMF WP/03/61)